There’s been a lot of media coverage lately about booming housing prices. Some are pointing to big institutional buyers, like REITs, as a source of the problem. We tend to disagree. Here’s why.

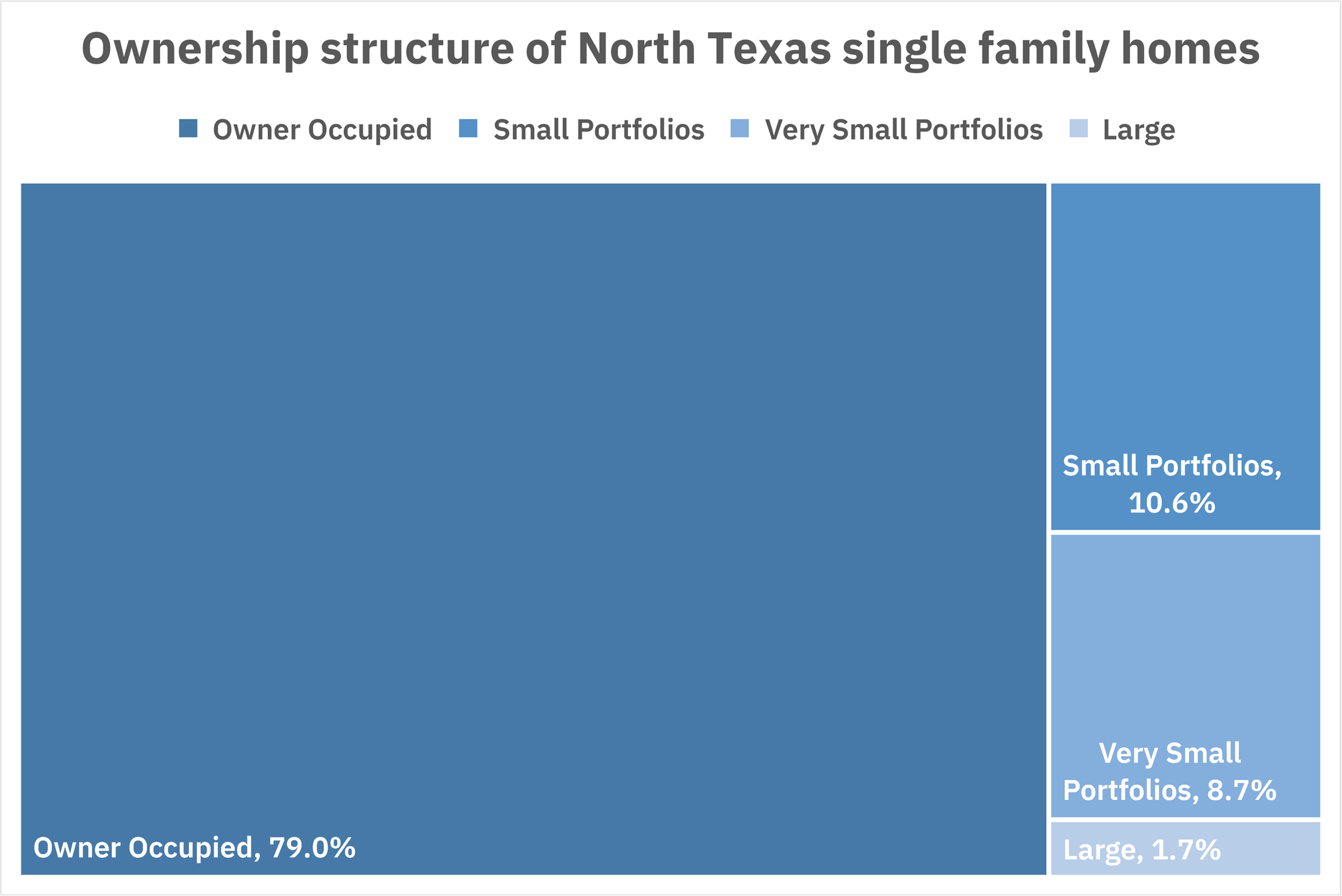

Big SFR buyers emerged on the scene in the early 2010s and started buying the many under-priced, distressed houses that appeared around the country after the 2008 crash. Since then, their presence has steadily grown. By our calculations, around 32,500 houses here in the Dallas-Fort Worth metroplex are held in “large” portfolios of 50 houses or more. That is only 1.7% of the market. Small portfolios of 2-50 houses account for another 10.6% percent. For this discussion, we’re interested in the big portfolios.

Big funds only own 1.7% of the homes in the Dallas-Fort Worth area, not really enough to exert much influence.

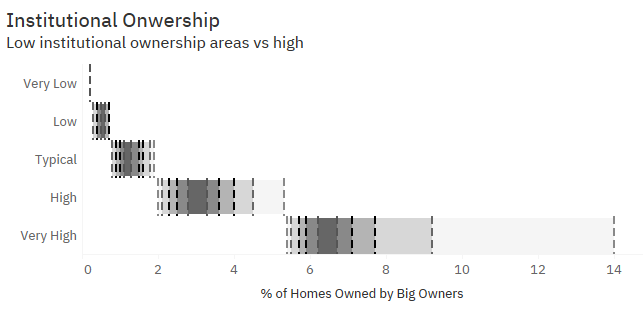

What is considered “high” institutional ownership?

What constitutes a high level of institutional ownership? We calculated this based on the ranges we see in the market. If more than about 5% of single family homes in a given location are institutionally owned, we categorize the location as having as “very high” institutional ownership.

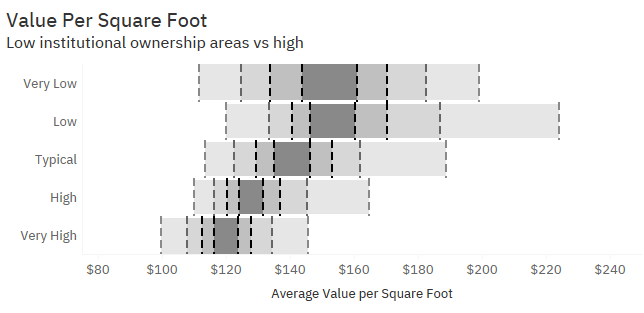

Ownership of single family rentals (SFRs) by big companies is concentrated in certain pockets of the Metroplex. Many of them are in moderately-priced areas.

What is considered “high” appreciation?

We built our own automated valuation model to estimate the value of every home in the market going back several years. Based on this, we can calculate how much prices went up in every area in great detail.

We can calculate how much prices went up in every area in great detail.

During the 2017-2020 time period, there was double-digit annual appreciation in certain pockets of the Dallas-Fort Worth area, which appear in reddish-magenta below. Some neighborhoods rose at 10% or more per year during that period. A quick look at the sales history of houses in these areas on any big-name real estate portal will confirm this.

Ominous — but misleading — correlations

When looking at the trends from a surface level, a lot of factors like tight inventory levels and appreciating prices seem to correlate well with high levels of big-fund SFR ownership.

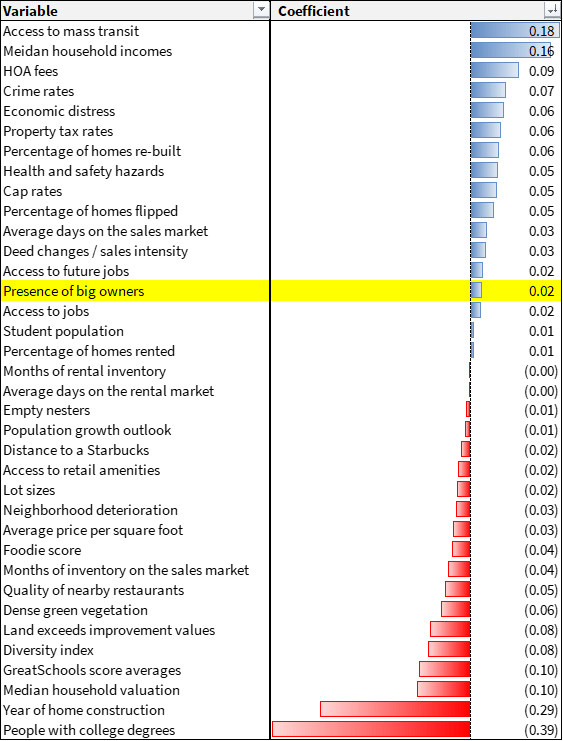

However, when we attempt to tease out the specific effect of big funds, by taking all factors together at once in a multiple regression, we find that the presence of big buyers explains only a very small part — if any — of the appreciation that happened in the market.

Correlation, not causation

Let’s start by looking at the relationship with individual factors.

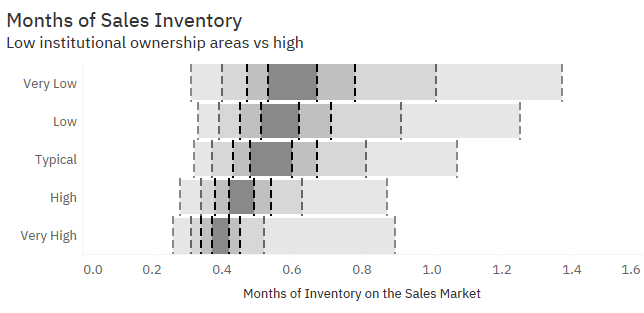

First, areas popular with institutional buyers do seem to have less inventory on the market, at least when considering what is available on the open market. Inventory is scarce everywhere, but seems to be more scarce in areas with a lot of big owners. This makes sense.

Darker areas are the center of the distribution.

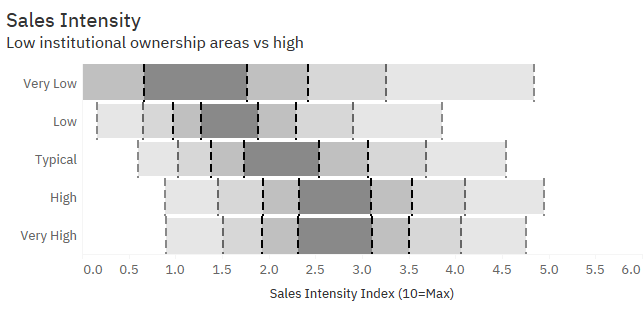

Looking at deed changes, which includes both on-market and off-market sales, the intensity of sales also tends to be higher in areas with a lot of institutional owners.

Darker areas are the center of the distribution.

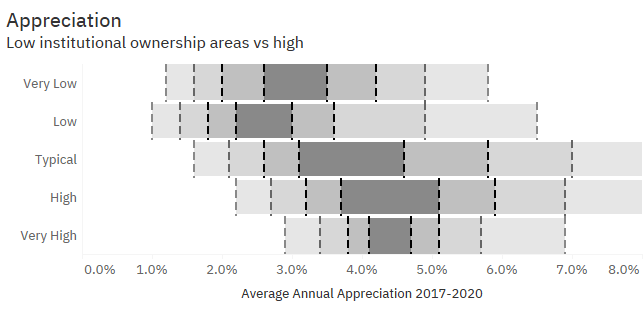

Also, pre-pandemic appreciation rates tended to be higher in areas with more institutional owners.

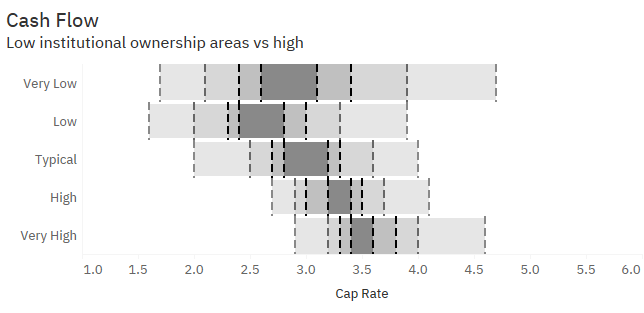

Cap rates are higher too where big funds are present, as they tend to gravitate toward areas with more cashflow potential. Of course, our cap rates are conservative because we load them with full rehab costs and other expense items. But the trend is there.

Darker areas are the center of the distribution.

Teasing out the effect of big funds

We put together a multi-factor model to try to tease out the effects of big funds from the effects of many other things that describe a given location. We did this at the block level to understand micro-level effects.

Our model explains about 79% of the variance in appreciation that occurred in the three-year period pre-pandemic. (Post-pandemic is a different story, for another time).

Homes owned by big companies showed a very limited effect on appreciation.

We ran several versions of the model with different variables, and the effect ranged from neutral to slightly positive.

Meanwhile, some appreciation drivers were unsurprising: access to transit, high incomes, and intensity of sales as measured by deed changes.

Others were more surprising: elevated levels of crime, distress, and the negative effect of high education levels. This is probably a reflection of the most rapid price growth in this period occurring in close-in areas, where even un-improved properties often doubled in value in the three years pre-pandemic.

We would expect to see a different result if examined over more than three years. But I chose this period of time as it represented pre-pandemic and the tail end of the SFR buying spree.

The buy box is getting smaller

Most institutional funds had a set of criteria on what made sense to buy, in order to get the best possible financial returns. This led them to buy in very specific areas. As the market tightens and prices rise, these areas are becoming smaller and rarer, making it hard to buy houses this way in large quantities.

Therefore, a shift toward development is taking place, with many new communities being purpose-built, from the ground up, as rentals. Development projects do not “compete” with buyers in the market to purchase homes, as they stay in the rental market from day one.

Therefore, we can expect big buyers to become even less relevant as a possible source of competition or appreciation in the market.

Methodology Notes

Our approach to developing an appreciation model is comprehensive. We built a machine learning model that calculates the price of every house at different points in time over the past few years. We then aggregate those to the block level and calculate changes across a moving window of the nearest 25 blocks, weighted by number of houses. We don’t simply use changes in median price as these don’t work at the micro level.